Table of Contents

What Is Islamic Finance?

In today’s financial world, many seek ethical and morally sound ways to manage money. Islamic finance provides a unique alternative by following Sharia (Islamic law) principles. Unlike conventional banking, it prohibits interest (riba), excessive uncertainty (gharar), and unethical investments. Whether you’re Muslim or simply interested in ethical banking, understanding Islamic finance can help you make better financial decisions.

Core Principles of Islamic Finance

Islamic finance operates under key Sharia-compliant rules:

- Prohibition of Riba (Interest)

- Earning or paying interest is strictly forbidden.

- Instead, profit-sharing (Mudarabah, Musharakah) and asset-backed financing (Murabaha) are used.

- Avoidance of Gharar (Uncertainty)

- Contracts must be clear—no hidden risks or ambiguity.

- This prevents speculative and gambling-like transactions (Maisir).

- Ethical Investments Only

- No funding for haram industries (alcohol, gambling, pork, weapons).

- Investments must benefit society.

- Asset-Backed Transactions

- Money must be tied to real assets (property, commodities).

- Prevents artificial inflation and financial bubbles.

How Islamic Finance Works: Common Products

1. Islamic Banking (No Interest Loans)

- Murabaha: Bank buys an asset (e.g., a car) and sells it at a markup (no interest).

- Musharakah: Partnership where profit/loss is shared (used in business financing).

2. Sukuk (Islamic Bonds)

- Unlike conventional bonds, Sukuk represent ownership in a tangible asset (e.g., real estate).

3. Takaful (Islamic Insurance)

- A cooperative system where members pool funds to support each other in need.

4. Islamic Mortgages (Ijara & Diminishing Musharakah)

- Ijara: Lease-to-own model (bank buys the house, rents it to you).

- Diminishing Musharakah: You and the bank co-own the property; you gradually buy their share.

Real-Life Examples from Islam

Hadith on Riba (Interest)

The Prophet (PBUH) said:

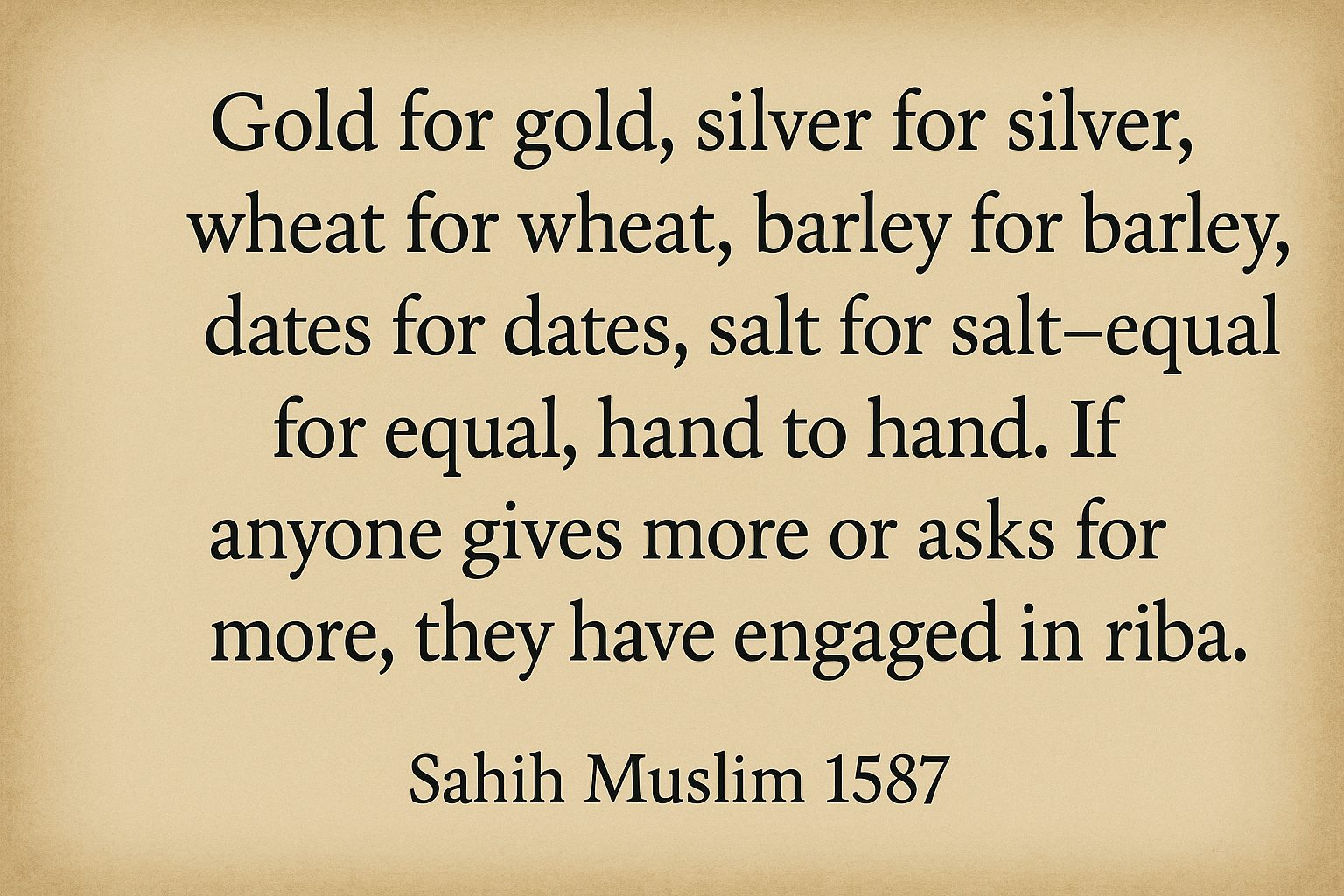

“Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates, salt for salt—equal for equal, hand to hand. If anyone gives more or asks for more, they have engaged in riba.” (Sahih Muslim 1587)

This teaches fair exchange—no exploitation in transactions.

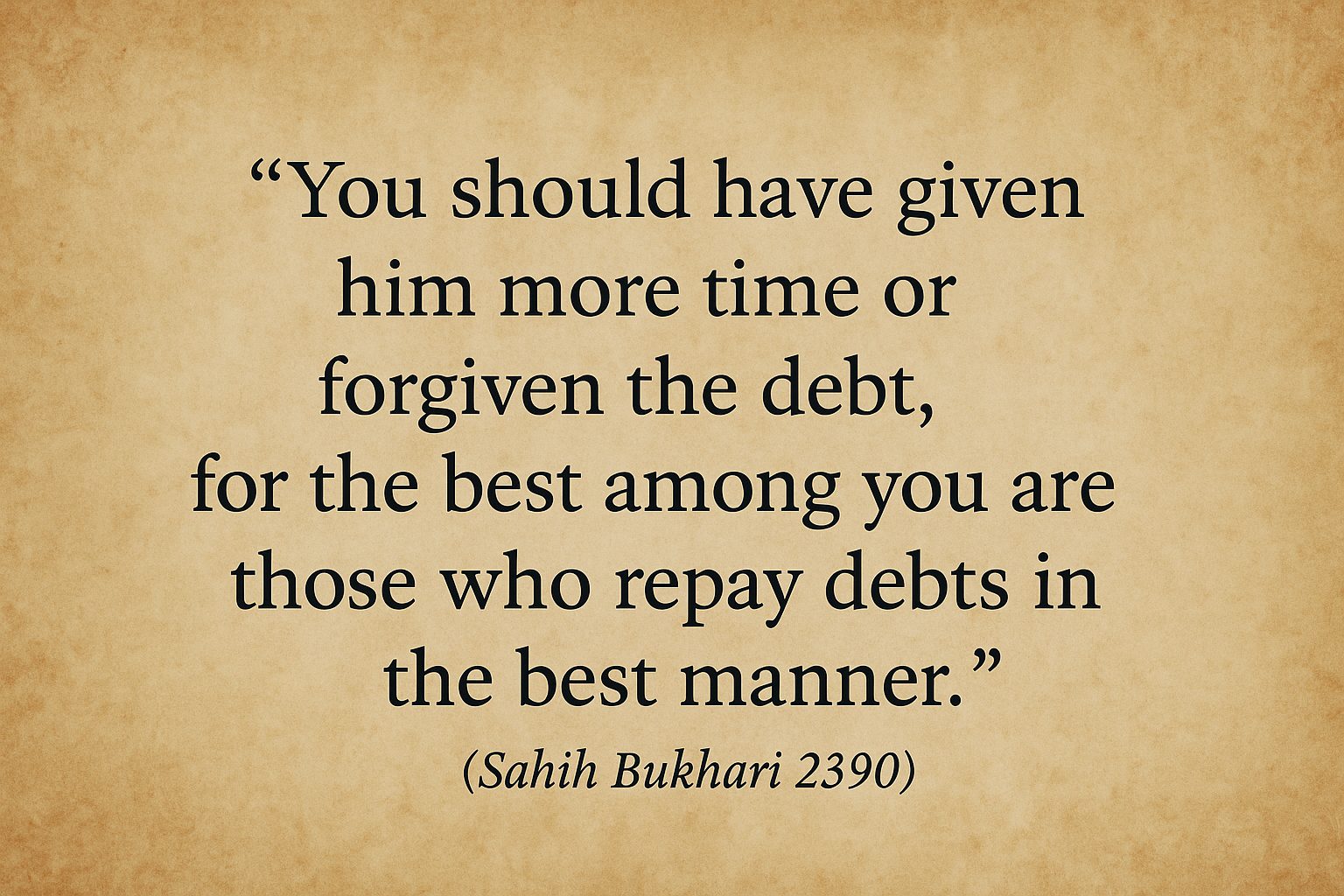

The Prophet (PBUH) and Debt Forgiveness

A debtor struggled to repay, but his creditor demanded harshly. The Prophet (PBUH) said:

“You should have given him more time or forgiven the debt, for the best among you are those who repay debts in the best manner.” (Sahih Bukhari 2390)

This highlights mercy in financial dealings, a core value in Islamic finance.

Umar ibn Al-Khattab (RA) and Market Ethics

Caliph Umar (RA) banned monopoly (Ihtikar) and price manipulation, ensuring fair trade—an early form of Islamic economic justice.

Why Choose Islamic Finance?

Ethical & Fair – No exploitation or harmful industries.

Stable & Low Risk – Avoids debt bubbles and speculation.

Socially Responsible – Encourages investments that benefit society.

Challenges and Growth of Islamic Finance

While Islamic finance is growing globally (over $3 trillion in assets), challenges remain:

- Limited Awareness – Many people still don’t understand Sharia-compliant banking.

- Regulatory Differences – Not all countries have supportive laws.

- Product Availability – Some regions lack Islamic banking options.

Yet, with increasing demand for ethical finance, the industry is expanding rapidly—especially in Malaysia, UAE, Saudi Arabia, and the UK.

Final Thoughts:

Whether you’re Muslim or simply seeking ethical banking, Islamic finance offers a fair, transparent, and risk-sharing alternative to conventional systems. By avoiding interest and unethical investments, it promotes financial justice—a principle deeply rooted in Islam.